In a significant development that could shape the future relationship between Artificial Intelligence (AI) and tax administration in India, the Punjab and Haryana High Court has quashed a GST Show Cause Notice (SCN) after finding that the notice appeared to have been prepared with the assistance of Artificial Intelligence without proper independent application of mind by the concerned tax officer.

The judgment, delivered in the matter of M/s SRO India v. State of Punjab & Another (dated 07 July 2026), has triggered an important debate regarding the permissible use of AI tools in quasi-judicial and adjudicatory proceedings under Indian tax laws.

Background of the Case

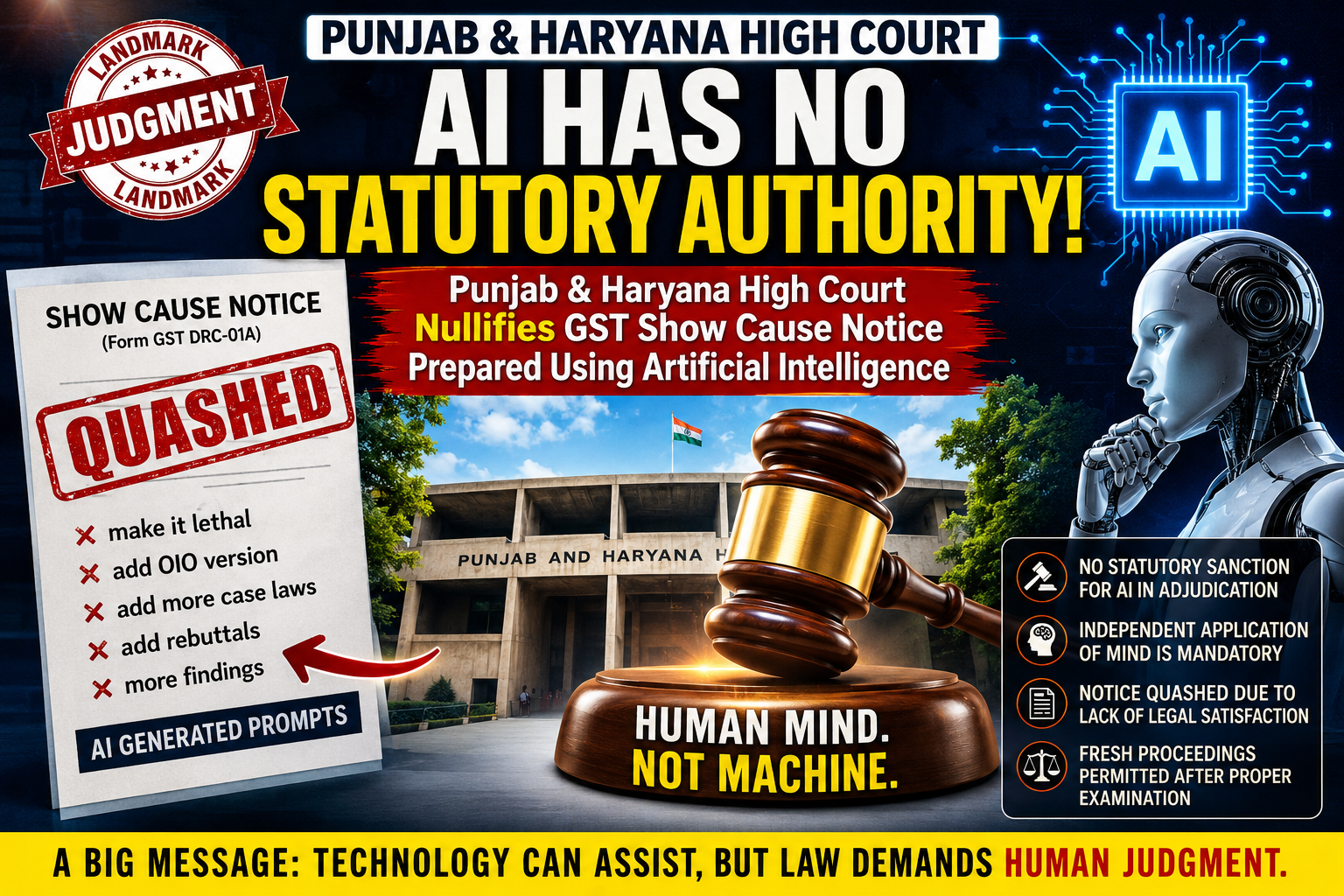

The petitioner, M/s SRO India, challenged a Show Cause Notice issued in Form GST DRC-01A under the Goods and Services Tax (GST) regime. The challenge was not based merely on the tax demand itself but on the manner in which the notice had been prepared.

During examination of the uploaded notice, several unusual phrases and drafting instructions were reportedly found embedded within the document. These included prompts such as:

- “Make it lethal”

- “Add OIO version”

- Suggestions to insert additional case laws, findings and rebuttals.

Such expressions are commonly associated with AI-assisted drafting platforms and large language model tools used for document generation.

The petitioner argued that these prompts clearly demonstrated that the tax officer had relied upon Artificial Intelligence to prepare the notice and had failed to independently analyze the facts and legal issues before issuing the statutory notice.

Department’s Defence

The State authorities submitted before the Court that these references had been uploaded accidentally and that the inclusion of such prompts was merely inadvertent.

However, the Court was not persuaded by this explanation.

The High Court observed that the contents and structure of the notice indicated reliance on AI-generated drafting assistance, raising serious concerns about whether the statutory authority had exercised independent judgment before initiating proceedings.

Court’s Observations

The Punjab and Haryana High Court emphasized an important legal principle:

A Show Cause Notice is not a mere procedural formality. It is the foundation of adjudication proceedings and must reflect the independent satisfaction and reasoning of the competent authority.

The Court held that:

- The GST law requires the proper officer to independently examine the facts.

- Issuance of notices cannot be a mechanical exercise.

- There is presently no statutory framework authorizing replacement of human decision-making with Artificial Intelligence in quasi-judicial functions.

- Any notice issued without proper application of mind becomes legally vulnerable.

Accordingly, the Court quashed the impugned Show Cause Notice and all consequential proceedings arising therefrom.

However, the Court granted liberty to the department to initiate fresh proceedings in accordance with law after independently examining the facts of the case.

Why This Judgment is Important

This ruling may become one of the earliest and most significant judicial pronouncements in India dealing directly with the use of Artificial Intelligence in tax administration.

The verdict does not prohibit the use of technology altogether. Rather, it draws a clear distinction between:

- Using AI as an administrative assistance tool, and

- Delegating statutory decision-making to AI systems.

The Court appears to have made it clear that while technology can assist officers, the final reasoning, satisfaction, and conclusions must come from the statutory authority itself.

Impact on GST Department and Tax Authorities

1. Increased Scrutiny of GST Notices

Taxpayers may now carefully examine GST notices and adjudication orders to determine whether they contain signs of mechanical drafting or AI-generated language.

Any indication that an officer has not independently applied his or her mind may become a ground for legal challenge.

2. Review of Internal Drafting Practices

GST departments across various states may now review their internal processes regarding:

- Drafting of notices,

- Use of AI tools,

- Standard templates,

- Automated legal research systems.

Authorities may issue fresh guidelines to ensure that officers verify and personalize notices before issuance.

3. Greater Accountability of Officers

This verdict reinforces the long-established judicial principle that quasi-judicial powers cannot be exercised mechanically.

Even if AI tools are used for research or drafting assistance, officers must ensure that every notice reflects independent reasoning and factual examination.

4. Potential Impact Beyond GST

The implications of this judgment are not confined to GST alone.

Similar principles may also affect:

- Income Tax proceedings,

- Customs adjudications,

- FEMA matters,

- Corporate regulatory actions,

- Labour and other administrative proceedings.

Any government authority relying excessively on AI-generated outputs without human review may face legal challenges.

Can AI Be Used in Tax Administration?

The answer appears to be Yes, but with limitations.

Artificial Intelligence can significantly improve efficiency in:

- Data analytics,

- Fraud detection,

- Risk profiling,

- Legal research,

- Draft preparation,

- Identification of suspicious transactions.

However, statutory functions such as:

- Formation of opinion,

- Recording of satisfaction,

- Issuance of notices,

- Adjudication of disputes,

must continue to remain human functions unless the legislature specifically provides otherwise.

The judgment effectively reiterates the legal principle that technology cannot replace statutory discretion.

A Warning Signal for the Era of AI Governance

The increasing use of AI in governance raises broader constitutional and administrative law concerns.

Questions may arise regarding:

- Transparency of AI systems,

- Accountability for errors,

- Bias in AI-generated outcomes,

- Due process rights of taxpayers,

- Validity of automated decision-making.

As governments increasingly adopt digital governance mechanisms, Indian courts may be called upon to define the legal boundaries of Artificial Intelligence in public administration.

The Punjab and Haryana High Court judgment may therefore become a foundational precedent in future litigation concerning AI-assisted governmental decision-making.

Conclusion

The decision in M/s SRO India v. State of Punjab & Another serves as an important reminder that while technology can assist governance, statutory powers must still be exercised by human authorities entrusted by law.

The ruling does not oppose innovation or Artificial Intelligence. Instead, it emphasizes that AI cannot substitute independent application of mind where the law requires a human authority to make decisions.

For taxpayers, the verdict offers an additional safeguard against mechanical and automated proceedings.

For tax administrators, it serves as a caution that efficiency and technological advancement cannot come at the cost of legality, fairness, and due process.

As Artificial Intelligence becomes increasingly integrated into governmental functions, this judgment may mark the beginning of a new era of judicial scrutiny over AI-assisted administrative actions in India.

Disclaimer:

This article is intended solely for educational, informational, and journalistic purposes. The contents are based on publicly available judicial information relating to the judgment in M/s SRO India v. State of Punjab & Another dated 07 July 2026. The article does not constitute legal, tax, or professional advice. Readers are advised to refer to the original judgment and consult qualified professionals before taking any action based on the information contained herein. The legal position may evolve through future judicial pronouncements, legislative amendments, or administrative clarifications.

Leave a Reply